I am posting before the close. So things might change after the close. So readers beware.

US INTEREST RATES

General Remarks:

In this post, I provided a thorough explanation concerning the rationale behind my use of two alternative definitions to appraise secondary reactions.

TLT is the iShares 20 years + Treasury bond ETF. More about it here

IEF is the iShares 7-10 years Treasury bond ETF. More about it here.

Thus, TLT tracks longer-term US bonds, whereas IEF tracks middle-term US bonds. A bull market in bonds entails lower interest rates. A bear market in bonds represents higher interest rates.

A) Market situation if one appraises secondary reactions not bound by the three weeks and 1/3 retracement dogma.

As I explained here, the primary trend was signaled as bullish on 7/22/22

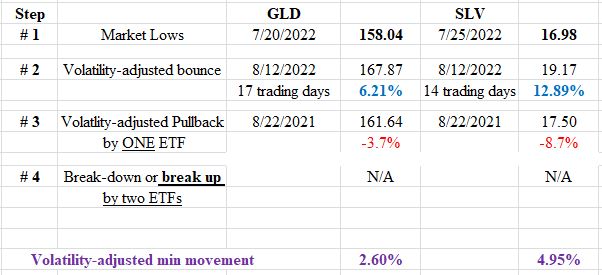

Following the 8/01/22 closing highs, a deep pullback followed until 8/24/22. Such a pullback has lasted until now 17 trading days which amply meets the time requirement for a secondary reaction against the primary bull market. As for the extent requirement, it has been fulfilled too, given that TLT and IEF declined more than the Volatility-Adjusted Minimum Movement (more explanations about VAMM here).

The Table below contains all the details

Now we are waiting for a rally lasting at least two trading days and exceeding the VAMM on at least one ETF to set up both ETFs for a potential primary bear market signal.

Therefore, now we are confronted with three alternatives:

a) Either the 8/01/22 closing highs are jointly broken topside by TLT and IEF, which will re-affirm the primary bull market.

b) or the 6/14/22 last recorded primary bear market lows are broken downside, which will signal a new primary bear market. This signal is unlikely to materialize but is our last resort stop-loss in case that the awaited 2 days rally does not occur, and the bonds keep falling like a knife.

c) As explained above, we get a two days rally exceeding the VAMM on at least one ETF, which will set up TLT and IEF for a potential primary bear market signal.

In the meantime, we wait and observe.

Below you have the updated charts. The brownish rectangles highlight the secondary reaction against the primary bull market.

B) Market situation if one sticks to the traditional interpretation demanding more than three weeks and 1/3 confirmed retracement to declare a secondary reaction.

The primary trend was signaled as bearish on 9/28/21. A more aggressive and legitimate interpretation would have signaled the bear market on 9/24/21. The explanations here.

The rally off the 6/14/22 closing lows lasted 32 trading days. Therefore, the time requirement for a secondary reaction has been met. As to the extent requirement, if we require 1/3 confirmed retracement of the previous bear swing, the retracement is around 25% for TLT and 41.5% for IEF. On the other hand, if we just require that the rally exceed the Volatility-Adjusted Minimum Movement (more explanations here), the extent requirement would have been met. While it’s up to each trader to make a judgment call, I consider the requirements for a secondary reaction fulfilled. The rally lasted 32 trading days, doubling the minimum time requirement of 15 days. Furthermore, percentage-wise the rally quadruples the VAMM for TLT and septuplicates the VAMM for IEF. Thus, I consider that the extent requirement is more than enough. This specific market juncture highlights that demanding at least a confirmed 1/3 retracement to consider the existence of a secondary reaction is flawed. I demolished such a myth in this post.

If we consider the rally ending on 8/1/22 as a secondary bullish reaction against the primary bear market, then the ensuing pullback has set up TLT and IEF for a potential primary bull market signal. The Table below contains all the relevant data:

So now the

situation is as follows:

a) If the 8/1/22 closing highs are jointly broken up, a primary bull market will be signaled.

b) If the

pullback continues lower and the 6/14/22 bear market closing lows are jointly

broken down, the primary bear market would be re-affirmed.

The charts below display the price action from the Bull market top on 12/3/21 till the bear market last recorded lows on 6/14/22 and the rally (blue rectangles) that followed. The small grey rectangles in the middle of the charts show a rally that did not qualify as a secondary reaction, and, hence, according to the Dow Theory, is to be disregarded.

The charts below focus on the most recent price action, namely the most recent rally (secondary bullish reaction against the primary bear market, shown with a blue rectangle) and the most recent pullback that set up both ETFs for a potential primary bull market (shown with a brownish rectangle). The blue horizontal lines highlight the secondary reaction highs, the relevant levels to be broken topside for a new bull market to be signaled.

Sincerely,

Manuel Blay

Editor of thedowtheory.com